The Cambridge Centre for Alternative Finance (CCAF), at the Judge School of Business at Cambridge University, has launched their annual research initiative pertaining to the global alternative finance industry. While in years past CCAF has staggered the research, this year they are commencing all at once, targeting the various regions around the world simultaneously including: the United Kingdom, Europe, the Americas, Asia and Africa.

The CCAF reports have emerged as the leading source for accurate data on innovations in finance such as crowdfunding, peer to peer lending (online lending), blockchain development and cryptocurrency. Regulators and policymakers from around the world have benefitted from the unparreleled insight into Fintech provided by the CCAF benchmarking reports.

Rotem Shneor, Associate Professor School of Business and Law University of Agder, Norway, who is co-leading the EU portion of the study, commented on this year’s research project;

Rotem Shneor, Associate Professor School of Business and Law University of Agder, Norway, who is co-leading the EU portion of the study, commented on this year’s research project;

“It is a pleasure and honor to once again join the excellent research team working on this important report. Previous reports have been the most comprehensive and reliable source for industry facts and figures. The European report provides quality well-researched information for anyone seeking to understand market dynamics, developments, challenges and opportunities in the alternative finance industry. As such, it is widely used by industry players for strategic decision making, by government officials for policy formulations, by educators in crowdfunding teaching and training, as well as by researchers who are inspired by the identified facts and gaps driving further research in a new emerging field.”

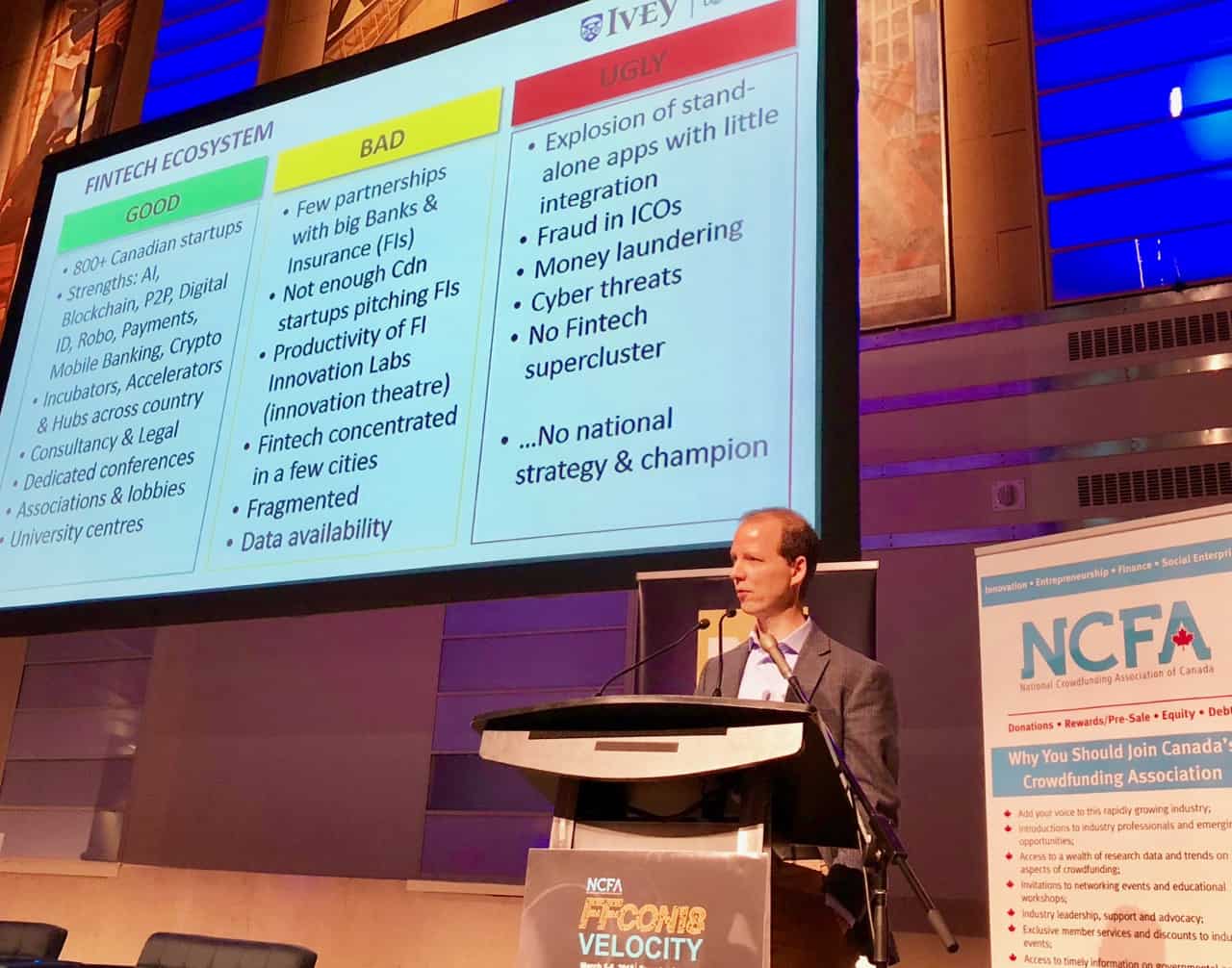

Michael King, an Associate Professor at Ivey Business School in Canada, is helping CCAF compile data in his country. He says that collecting accurate data on the state of alternative finance in Canada is crucial for establishing the credibility of this funding source with regulators, politicians, investors, and borrowers.

Michael King, an Associate Professor at Ivey Business School in Canada, is helping CCAF compile data in his country. He says that collecting accurate data on the state of alternative finance in Canada is crucial for establishing the credibility of this funding source with regulators, politicians, investors, and borrowers.

“Without reliable data showing its importance, marketplaces and online platforms cannot hope to be viewed as legitimate partners. The 2018 survey is well-timed to contribute to the review of Canada’s Financial Sector Framework, which will wrap up in 2019, particularly the debate over open banking”.

[clickToTweet tweet=”The 2018 survey is well-timed to contribute to the review of Canada’s Financial Sector Framework, which will wrap up in 2019, particularly the debate over open banking #Fintech” quote=”The 2018 survey is well-timed to contribute to the review of Canada’s Financial Sector Framework, which will wrap up in 2019, particularly the debate over open banking #Fintech”]

Diego Herrera, Financial Markets Specialist at the Inter-American Development Bank, described the CCAF research as vital;

“This research is very important for Latin America and the Caribbean for mainly two reasons: First, as of 2015 the region knew that the Fintech ecosystem, in particular Alternative Finance, was growing up, but nobody knew to what extent or its size. The first version of the study delivered clear data on the segments for the alternative finance ecosystem on volume, type of clients, size per country, among other relevant numbers. The following study and its depp dive in Mexico and Chile delivered trends on data and also details such as price, reasons to use platforms against the traditional financial sector, among others. Second, as a continued effort, this study is the only source in the region to determine what researchers and the industry would like to know on the AF industry, creating a large value added for everyone. It is not just an accounting on the number of platforms but rather a collection of useful data on what the vertical is offering for the region in terms of inclusion and supply of financial instruments.”

Dr. Naoyuki Yoshino, Dean at Asian Development Bank Institute, said that expanding access to finance is an important development objective in many Asia-Pacific countries;

“Fintech holds great promise to accelerate and facilitate the achievement of such access. This survey will provide an important database from which to develop policy recommendations to promote financial inclusion while safeguarding financial stability and maintaining consumer protection.”

Professor Shenglin Ben, Dean of Academy of Internet Finance at Zhejiang University added that alternative finance has experienced vigorous growth in recent years around the globe. Various business models are flourishing in different regions and markets. In particular, marketplace lending and crowdfunding are key parts of alternative finance that have gone through rapid and dynamic development creating highly diversified business models – especially in the Asia Pacific region.

“I am very glad that the Cambridge Center for Alternative Finance (CCAF), the Academy of Internet finance, Zhejiang University (AIF) and the Asian Development Bank Institute (ADBI) are working jointly to conduct the 2018 Asia Pacific alternative finance survey, aiming to provide useful insights for both policy makers and practitioners in the area of alternative finance. We are very grateful to your kind support and participation.”

CI had a chance to speak with Bryan Zhang, Executive Director of CCAF, and Tania Ziegler, Senior Research Manager at CCAF, on the forthcoming research project. I asked them why they decided to complete their annual research in one fell swoop this year.

CI had a chance to speak with Bryan Zhang, Executive Director of CCAF, and Tania Ziegler, Senior Research Manager at CCAF, on the forthcoming research project. I asked them why they decided to complete their annual research in one fell swoop this year.

Zhang and Ziegler explained that in previous years they would launch 5 or 6 different surveys that were region blocked. But with so many platforms operating in multiple jurisdictions and operating more than one model, they realized that they weren’t capturing what was really happening globally. The emergence of cross regional activity is a critical finding they haven’t quite teased out in our previous reports, changing the survey format should help rectify this.

[clickToTweet tweet=”The emergence of cross regional activity is a critical finding #Fintech” quote=”The emergence of cross regional activity is a critical finding #Fintech”]

So other than the timing of the research, what has changed in the Fintech world?

“For five years, we have recorded impressive growth and documented how alternative finance models have developed and become more sophisticated,” shared Zhang. “In that time, we have seen alternative finance become a global phenomenon [they are now tracking platform activity in over 170 countries], with greater interconnectivity at a cross regional level. As platforms (and the models they operate in) become more sophisticated, they are increasingly becoming borderless as well.”

[clickToTweet tweet=”As #Fintech platforms become more sophisticated, they are increasingly becoming borderless as well” quote=”As #Fintech platforms become more sophisticated, they are increasingly becoming borderless as well”]

Having now tracked alternative finance for five years, and from this relatively short perspective, the Centre has noted an emerging industry that has progressed quickly. Where once there were only handful of early adopters and innovators in a given country, they now see an “altfin” landscape that is growing rapidly, with an exponential number of new platforms driving competition and introducing new products.

In many regions (the EU, UK, USA) the Centre is also seeing their first cases of consolidation, but with continued diversification of products and services to customers.

In recent years, they have documented a concerted effort to streamline and innovate investment processes, and to introduce new technologies (blockchain, gamification, etc) for the products on offer.

Yet, despite displaying continuous growth, the altfin landscape has not reached its potential.

Yet, despite displaying continuous growth, the altfin landscape has not reached its potential.

“Key challenges persist relating to market education (both for incumbent finance providers and the consumers who might use an altfin platform) and integration of Fintech-friendly regulation into long-established regulatory systems (the caveat here is that this varies significantly across countries),” stated Ziegler. In recent years, we have seen a much greater emphasis on regulatory innovation (in certain countries), with an emphasis on activity-appropriate approaches towards alternative finance models. This has gone hand-in-hand with policy directives for increased SME access to finance, financial inclusion, etc. Five years ago, there was a heavy-dose of skepticism when discussing alternative finance. From what we have observed, the tides have changed, with greater willingness to enable policies or regulatory frameworks that include fintech operators.”

While it may be hard to predict, I inquired as to what they expect for this years report in the various regions (UK / Europe / Americas (US) and Asia / Pac).

“In Latin America, we expect to see continued exponential growth, especially in countries where there has been a concerted effort to lead regulatory innovations such as Mexico,” Zhang explained. “In the US, we suspect there will be further consolidation but considerable innovation in terms of products and services provided by alternative finance platforms. In Asia-Pacific, there has been a significant emphasis on regulatory sandboxes and innovation. We suspect that this will translate to stronger alternative finance markets and rapid growth across the region.”

Zhang said that in Europe cross-regional investment have increased considerably.

“We suspect that more and more platforms will pursue an international strategy and service investors and fundraisers across the region. In the UK, we are likely to see further consolidation in terms of the number of platform operators but significant growth in terms of volume,” added Zhang. “With policy initiatives to encourage SME-access to finance and data-sharing initiatives, the service provided to end-users is likely to develop in encouraging ways.”

And what about the hot topic of blockchain (distributed ledger technology – DLT) and its impact on alternative finance?

“To date, it hasn’t had too large a material impact, with only a handful of platforms allowing for investment in cryptocurrencies,” said Ziegler. “That said, the intellectual impact has been considerable, with many platforms exploring a blockchain or DLT application to streamline their processes and enhance their product offerings. For instance, in our Expanding Horizons report, we noted that many platforms are focusing their R&D on distributed ledger technology related to client-money tracking, verification and due-diligence processes and in issuing shares/potential returns.”

[clickToTweet tweet=”We have noted a considerable increase in female participation, with more women-led campaigns and a greater number of women investors. We also have noted a significant increase in small businesses that are able to receive funding #Fintech” quote=”We have noted a considerable increase in female participation, with more women-led campaigns and a greater number of women investors. We also have noted a significant increase in small businesses that are able to receive funding #Fintech”]

So is Fintech living up to its ambitious objective of providing access to capital and services to a far wider population?

“In the last five years, we have noted a considerable increase in female participation, with more women-led campaigns and a greater number of women investors participating in the landscape,” Ziegler shared. “We also have noted a significant increase in micro and small-businesses that are able to receive funding where a more traditional facility was not possible. Based on this, our observations would indicate that, yes, fintech is a net-positive towards access to capital and services.”

Zhang said the reality is that they don’t have enough data yet to fully back this claim.

“To rectify this, our 2018 survey includes a few additional questions to help us understand the impact of alternative finance vis-à-vis financial inclusion, especially towards unbanked/underbanked populations,” stated Zhang.

[clickToTweet tweet=”Our 2018 survey includes a few additional questions to help us understand the impact of alternative finance vis-à-vis financial inclusion, especially towards unbanked/underbanked populations #Fintech” quote=”Our 2018 survey includes a few additional questions to help us understand the impact of alternative finance vis-à-vis financial inclusion, especially towards unbanked/underbanked populations #Fintech”]

For Fintech platforms that are participating in the CCAF Research please see the various links to the surveys below. Please note: As in years past, all information will be aggregated and your information will remain anonymous.

THE GENERAL LINK (APPLICABLE TO ALL PLATFORMS GLOBALLY)