The recent changes in the retail equity crowdfunding regulatory environment make this a useful time to take stock of the international landscape and compare regimes between countries. Some countries have moved faster than others, and different countries have taken different approaches to regulation, ranging from very liberal to very protectionist.

The lines of what constitutes “retail crowdfunding” and what constitutes a public or private offer have become blurred. This analysis focuses on options available to issuers under reduced disclosure obligations (versus a prospectus), which are allowed to be marketed to “ordinary” investors – as in, those who do not pass any kind of “sophisticated” or “high net worth” threshold.

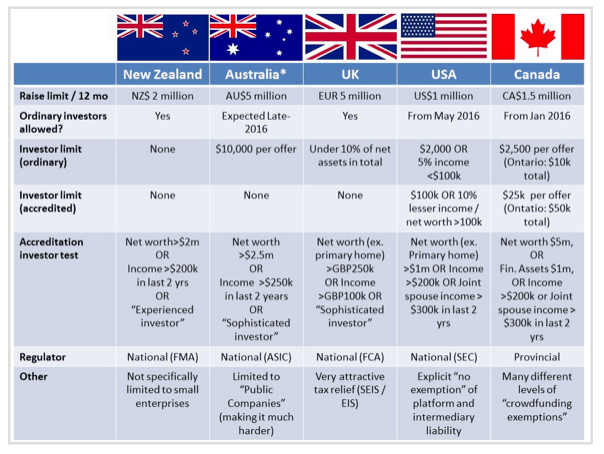

The table below summarizes the state of retail equity crowdfunding in the English-speaking countries of the OECD. Note that due to the complexity in the USA and Canada, it is impossible to cleanly provide detailed information on their various exemptions, so for these countries I am showing the regimes most in keeping with the spirit of retail equity crowdfunding – Title III in the US, and the “Crowdfunding Exemption 45-108” in Canada.

* Australia’s rules as displayed here are as proposed.

New Zealand

New Zealand enabled retail equity crowdfunding around 18 months ago, as part of a wide-ranging overhaul of the country’s entire investment and securities laws.

New Zealand enabled retail equity crowdfunding around 18 months ago, as part of a wide-ranging overhaul of the country’s entire investment and securities laws.

Since the first offer closed in the latter part of 2014, equity crowdfunding has grown into an established part of New Zealand’s alternative finance landscape, with substantial media attention and traditional angel investors now looking to participate as lead investors in equity crowdfunding offers. Four platforms have helped raise over NZ$16 million to the end of January 2016 across a wide variety of sectors.

New Zealand is regulated by the Financial Markets Authority, which took a liberal stance to the implementation of equity crowdfunding. There are no limits on what a retail investor can invest in each offer, and no specific disclosure requirements for issuers. Despite initial misgivings that low-quality issuers would take advantage of a regime that some saw as “lax”, New Zealand’s market has proved to be remarkably self-policing; the platforms heavily curate the issuers before they go live, as they realize it is in their own long-term interest to gain a reputation for bringing high-quality companies to the market so as to attract and retain a high-quality investor audience.

Australia

Despite retail equity crowdfunding being on the horizon for many years, Australia has not yet passed the enabling legislation – so as of right now, current Australian regulations limit the scope of equity crowdfunding to wholesale and sophisticated investors.

Despite retail equity crowdfunding being on the horizon for many years, Australia has not yet passed the enabling legislation – so as of right now, current Australian regulations limit the scope of equity crowdfunding to wholesale and sophisticated investors.

The timeframe has been pushed back several times, but in December 2015, the draft legislation was finally tabled. The proposed rules have been roundly criticized by industry participants as being overly onerous for issuers. The most important point of consternation is the restriction of retail equity crowdfunding to only be possible for public companies – distinct from the simpler and less burdensome private company structure that early stage ventures prefer. Essentially, this means issuers will need to convert to an unwanted company structure if they want to use equity crowdfunding as proposed, with all the administrative expense and disclosure that comes with it, making retail equity crowdfunding much more difficult for early stage companies to justify.

Also, the existing Corporations Act, passed into law before crowdfunding was conceived, restricts private companies to having no more than 50 shareholders, so even if the government would do an about-face on the public/private company issue, retail equity crowdfunding would also require this 50 shareholder limit to be lifted to enable the number of shareholders that would be naturally expected from a public crowdfunding offer.

United Kingdom

The UK has several years of operating history and is one of the most developed equity crowdfunding markets in the world with over £140 million raised. The UK’s momentum has been significantly helped through the generous tax incentives offered by the Seed Enterprise Investment Scheme (SEIS – for very early stage companies) and the Enterprise Investment Scheme (EIS – for somewhat later stage companies). Effectively, investors are able to write off tax liability if they invest in equity crowdfunded companies that qualify (and almost all do). Under SEIS for example, an individual investing £1,000 can claim £500 tax relief, and a further tax write-off in the event the company failed, dependent on their tax rate. Capital gains exemptions also apply for companies that go on to achieve a successful exit – therefore, an investor can gain £1,000 of virtually tax-free upside exposure, and is subject to less than half of the downside risk due to the tax write-off.

The UK has several years of operating history and is one of the most developed equity crowdfunding markets in the world with over £140 million raised. The UK’s momentum has been significantly helped through the generous tax incentives offered by the Seed Enterprise Investment Scheme (SEIS – for very early stage companies) and the Enterprise Investment Scheme (EIS – for somewhat later stage companies). Effectively, investors are able to write off tax liability if they invest in equity crowdfunded companies that qualify (and almost all do). Under SEIS for example, an individual investing £1,000 can claim £500 tax relief, and a further tax write-off in the event the company failed, dependent on their tax rate. Capital gains exemptions also apply for companies that go on to achieve a successful exit – therefore, an investor can gain £1,000 of virtually tax-free upside exposure, and is subject to less than half of the downside risk due to the tax write-off.

The UK is one of the few places with enough operating history to have seen successful exits and failures.

- Soshi Games were the victim of market trends. They were in the business of creating paid-for mobile games, but soon after raising, customers everywhere began to expect mobile games to be free, which killed their business model. They were put into liquidation in September 2015.

- Camden Brewery was bought out in a trade sale by brewing giant AB InBev for £85 million in December 2015, a 70% increase over its crowdfunded valuation from April, representing a good result due to a short time horizon.

Like New Zealand, the UK regulators have taken a reasonably light-touch approach, with no caps to what an issuer can raise other than the European Union non-prospectus maximum of EUR 5 million, and only a broad restriction of 10% of non-home assets for what investors can contribute to equity crowdfunding overall. The result has been the platforms have developed their own levels of disclosure and best practice to enhance their reputation and attract the best companies and investors – for example, Syndicate Room requires an approved lead investor for every deal they put on their platform, and this effectively vets the companies wishing to raise, their offer terms, and their valuations more effectively than prescribed disclosure can.

United States

The United States system is complex, with different carve-outs for equity crowdfunding depending on the amount raised, and state-specific exemptions under various rules. Title II of the JOBS Act enabled crowdfunding for accredited investors.

Regulation A+ updated the Securities Act of 1933. So long as a disclosure document is reviewed by the SEC, it allows for raises of up to US$20 million under “tier 1” and a more disclosure-heavy “tier 2” structure including annual audits which allows for raises up to US$50 million. Importantly, non-accredited investors are allowed to participate in Reg A+ offers.

The Title III rules will allow retail equity crowdfunding for even earlier-stage issuers. US-domiciled companies will be able to raise up to US$1 million in any 12 month period through online crowdfunding platforms. Notably, investment companies and special purpose vehicles are excluded from Title III, while the UK allows such structures.

The Title III rules will allow retail equity crowdfunding for even earlier-stage issuers. US-domiciled companies will be able to raise up to US$1 million in any 12 month period through online crowdfunding platforms. Notably, investment companies and special purpose vehicles are excluded from Title III, while the UK allows such structures.

Investor protection will be enhanced through the ability of platforms to subjectively curate the companies that come through their door. A remaining concern, particularly in a litigious place like the US, is the explicit non-exemption of liability for crowdfunding platforms and other advisors – in the event a company fails (which is an acknowledged possibility in practically every early stage venture), investors are not excluded from bringing actions against the market participants that helped bring that failed company to market. This risk of legal action could be reflected in higher expense to issuers, and fewer platforms and advisors being willing to take the risk of becoming involved with Title III raises.

Under Title III, audited financial statements will only be required for companies doing their second and subsequent raises, and even then only if they are raising above US$500,000. Other disclosure required includes background on company directors, a description of the business, use of proceeds, risk factors and related party transactions. These disclosure requirements are all reasonable and in line

Canada

Canada’s rules are the most complicated still, as they are imposed by the various provinces rather than a single nationwide regulatory body. Therefore, with 13 different regulators rather than 1, it is difficult to provide a succinct summary of all the nuance of Canada’s rules. Efforts to harmonize these rules are ongoing, but investment limits and exact disclosure requirements still vary between provinces.

Canada’s rules are the most complicated still, as they are imposed by the various provinces rather than a single nationwide regulatory body. Therefore, with 13 different regulators rather than 1, it is difficult to provide a succinct summary of all the nuance of Canada’s rules. Efforts to harmonize these rules are ongoing, but investment limits and exact disclosure requirements still vary between provinces.

All provinces currently allow Accredited Investors and Family, Friends and Close Business Associates to invest without requiring a prospectus. As far as retail investors go, there are two main regimes under which equity crowdfunding portals can make offers available:

- The “Offering Memorandum Exemption” 45-106, which allows for an uncapped level of capital to be raised from non-accredited investors, but must be accompanied by an offering memorandum which is not so complicated as a full prospectus, but still burdensome – it requires audited financial statements, which must continue to be filed on an ongoing basis, as well as a schedule post-raise explaining how offer proceeds were spent. According to Canadian platform SeedUps, this level of disclosure makes this regime more appropriate for companies wishing to raise over CA$2 million.

- The “Crowdfunding Exemption” 45-108, came into effect in January 2016 in Ontario, Quebec, Saskatchewan, Nova Scotia, Manitoba and New Brunswick. This offers companies wishing to raise up to CA$1.5 million an even more streamlined offering document, and it is this regime under which early stage ventures are likely to prefer.

Certain provinces offer various additional possibilities for lower levels of capital raises. With the recent movement in Canadian regulations, we will see retail equity crowdfunding kick off shortly. The various platforms are already busy conducting roadshows to educate the market.

Gaining Momentum

Equity crowdfunding is gaining momentum and has the potential to transform the funding landscape for both issuers and investors. However, in order to for it to become a global game-changer, it requires supportive legislation to facilitate the growth of platforms, investor audiences and high-quality companies. The countries that get their laws right will reap the rewards of a re-energized entrepreneurial economy, while those that impose too much burdensome regulation will be left behind. The lessons from New Zealand and the United Kingdom shows that competitive pressures between crowdfunding platforms result in market best practice evolving even in the absence of prescriptive regulation. As Canada, the US and (eventually) Australia bring retail equity crowdfunding into their landscapes, it will be interesting to see how their more tightly-regulated approach works in comparison.

Equity crowdfunding is gaining momentum and has the potential to transform the funding landscape for both issuers and investors. However, in order to for it to become a global game-changer, it requires supportive legislation to facilitate the growth of platforms, investor audiences and high-quality companies. The countries that get their laws right will reap the rewards of a re-energized entrepreneurial economy, while those that impose too much burdensome regulation will be left behind. The lessons from New Zealand and the United Kingdom shows that competitive pressures between crowdfunding platforms result in market best practice evolving even in the absence of prescriptive regulation. As Canada, the US and (eventually) Australia bring retail equity crowdfunding into their landscapes, it will be interesting to see how their more tightly-regulated approach works in comparison.

Nathan Rose is the Director of Assemble Advisory, a consultancy for companies wishing to pursue investment crowdfunding campaigns. Assemble Advisory assists with picking the right platform, putting together offer content and financial models, allowing companies to raise money sooner.

Nathan Rose is the Director of Assemble Advisory, a consultancy for companies wishing to pursue investment crowdfunding campaigns. Assemble Advisory assists with picking the right platform, putting together offer content and financial models, allowing companies to raise money sooner.